Transforming Real Estate Division During a Financial Crisis: Key Lessons for 2025

Feb 25, 2025

Transforming EMC Mortgage Real Estate Services’ REO Division During the Financial Crisis: A First-Person Account by Matt Slonaker

Sources used: My monthly letters, vision and strategic plans, reports and stats

As Senior Vice President at EMC Mortgage Real Estate Services, Inc., I found myself at the helm of our Real Estate Owned (REO) division during one of the most tumultuous periods in financial history—the 2008 global financial crisis. The collapse of the housing market, triggered by widespread mortgage defaults and the subprime meltdown, presented unprecedented challenges for EMC, a subsidiary of Bear Stearns and later integrated into JPMorgan Chase after its acquisition. Our REO division, tasked with managing and liquidating distressed real estate assets, became a critical battleground for stabilizing losses, driving value recovery, and positioning EMC as a leader in asset management. Here’s how we transformed our strategy and executed our plan during this crisis, in my own voice.

Navigating the Storm: The Context of 2008

When the financial crisis hit, the REO market was drowning in inventory. Foreclosures skyrocketed, and banks like Bear Stearns—EMC’s parent company—were left holding vast portfolios of unsellable properties. As newly appointed Senior Vice President, I saw the writing on the wall: our traditional approach to REO sales wasn’t going to cut it. We were managing properties as isolated transactions, but the scale of the crisis demanded a complete overhaul. Our goal wasn’t just to sell distressed assets—it was to maximize recoveries, reduce costs, and position EMC as a forward-thinking partner for JPMorgan Chase, our ultimate parent company after Bear Stearns’ collapse in March 2008.

I knew we had to move quickly. The market was chaotic, with plummeting property values, extended timelines for liquidation, and mounting pressure from stakeholders to mitigate losses. Our division, with its 87 employees and specialized teams, was ready to pivot—but it required bold vision, data-driven strategies, and a willingness to innovate under pressure.

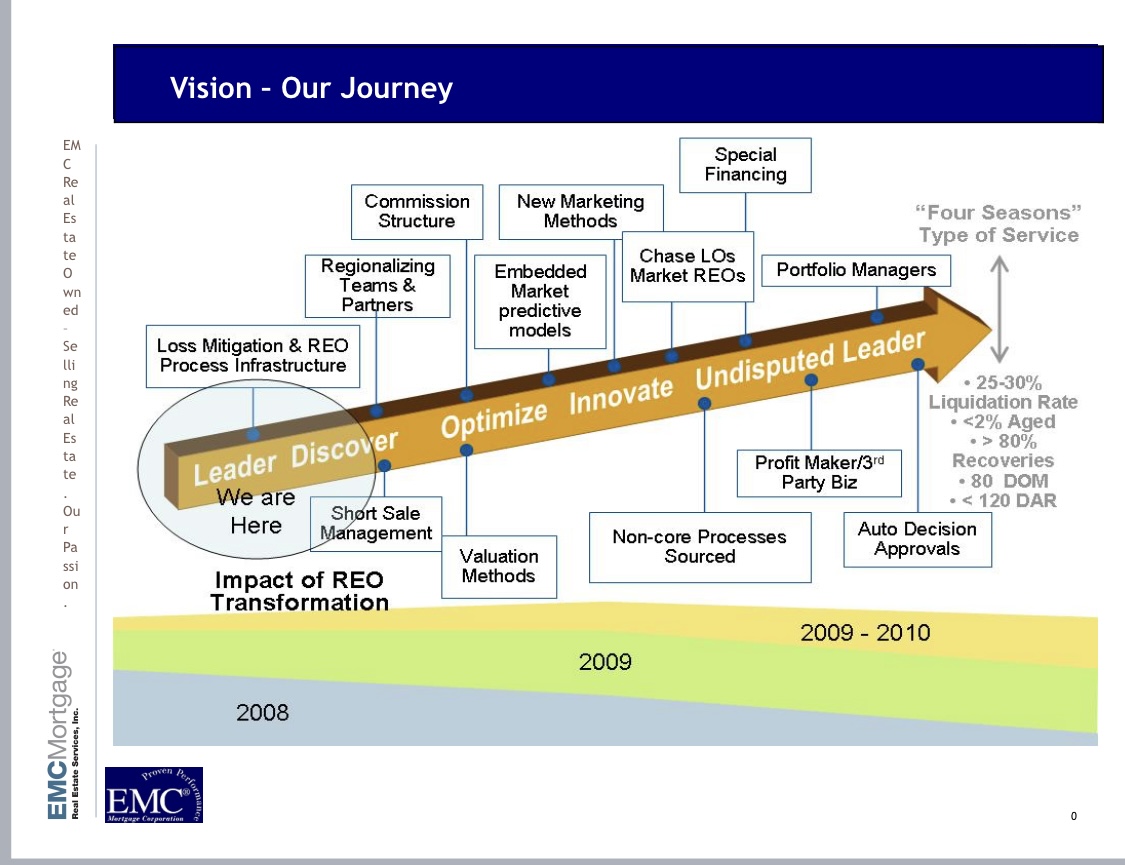

Our Vision: From Traditional REO to Portfolio and Consumer-Centric Leadership

My first step was to redefine our vision. We couldn’t just be a “traditional REO sales” operation, passively listing properties and hoping for buyers. I pushed for a transformation into a portfolio manager and consumer service model, focusing on selling distressed real estate while also cross-selling JPMorgan Chase financial products. This dual approach wasn’t just about survival—it was about creating a competitive edge.

Our mission became clear: manage national real estate portfolios better than anyone else in the industry. We aimed to reduce the cost of service while increasing sales and maximizing value recoveries. Accountability and ownership had to increase internally, and I leaned heavily on analytics and market intelligence to drive performance across sales and management levels. This wasn’t just a reactive strategy—it was a proactive one, designed to position EMC as a leader even in the depths of a crisis.

Key Components of Our Strategic Plan

We broke our strategy into actionable components, each designed to address specific pain points in the REO process during the financial crisis. Here’s how we approached it:

1. Sales Growth: Targeting 3,000 Liquidations Per Month

In October 2008, we were liquidating about 2,440 assets monthly, with a 24.88% liquidation ratio. That wasn’t enough. I set an ambitious target: exceed 25% of our total REO portfolio monthly, aiming for 3,000 sales per month by the first quarter of 2009. To achieve this, we introduced auction-style marketing, partnered with a lender liquidation company (e.g., LenderMustSell.com), and implemented performance incentives for our teams. We also leveraged mass marketing strategies, piloting programs in California, Nevada, Arizona, and Florida, with plans to expand. By driving competitive bidding early in the timeline, we saw sales increase by 111% from the previous year, and I knew we were on the right track.

2. Timeline Management: Reducing Days REO to Under 163 Days

One of our biggest challenges was the time it took to move properties from foreclosure to sale. In October 2008, our average days REO stood at 162, down from 195 the previous year, but still too high. I targeted reducing this to under 163 total days, with days on market under 115 and eviction timelines under 60 days. We implemented aged asset controls, regionalized service providers, and streamlined processes like agent assignments and evictions. Assigning listing agents immediately after boarding new REOs and coordinating second broker price opinions (BPOs) through valuation vendors helped us enhance accountability and speed up listings. By regionalizing our portfolio and adjusting our outsource/in-house strategy, we improved efficiencies and reduced costs, shaving days off our timelines.

3. Financials and Value Recovery: Mitigating Losses and Enhancing Recoveries

The crisis had driven property values down dramatically—sales prices compared to appraised values at loan origination were hovering around 50% in late 2008. Our goal was to reduce loss severity to under 59% and enhance value recoveries to exceed 68% of pre-foreclosure BPO values, while maintaining sales prices at over 90% of original anticipated sales prices. We introduced repair strategies in select metropolitan statistical areas (MSAs), used analytics to inform pricing, and doubled down on retail “auction-style” marketing to create competitive bid situations. By October 2008, our sales price to original anticipated sales price hit 91.91%, and net proceeds to REO sales price reached 88.21%—the second-highest ratios in six months. These gains, though modest, were critical in a declining market.

4. JPMorgan Chase Cross-Selling: A Customer-Centric Approach

As part of our integration with JPMorgan Chase, I saw an opportunity to align our REO sales with Chase’s broader financial offerings. We developed a leading customer service and sales approach, training our teams to cross-sell Chase products like mortgages, banking services, and insurance alongside REO assets. This wasn’t just about meeting quotas—it was about building long-term relationships with buyers, many of whom were navigating their own financial hardships. By positioning EMC as a trusted partner, we not only boosted sales but also strengthened our ties with Chase, ensuring our division’s relevance in the post-crisis landscape.

5. Talent Development and Innovation

I knew our people were our greatest asset, especially in a crisis. We invested heavily in training programs to ensure our 87 employees were equipped to handle the complexities of distressed asset management. We recruited top talent, implemented performance incentives, and rolled out quarterly innovations to differentiate our services. For instance, we developed the LenderMustSell.com platform, which generated over 35% of our leads through web and email campaigns by late 2008. We also regionalized our portfolio by geography and risk, segmenting by MSAs and zip codes to prioritize high-volume areas and reduce costs through direct sales in our “footprint” regions.

Challenges and Adaptations

The financial crisis threw curveballs at every turn. Property values continued to decline, with sales prices compared to appraised values dropping to 49.72% in October 2008 from 50.98% the previous month. Evictions and title issues slowed our timelines, and stakeholder pressure to cut costs while maximizing recoveries was intense. I worked closely with our executive team, including David Little, our Executive Vice President, and regional leaders like Teresa Nixon, Dena Grimes, and Rod Telles, to adapt our strategies. We regionalized our operations, adjusted our outsource model, and placed additional inspectors and property preservation teams to oversee assets centrally. By November 2008, we were piloting national rehab programs on outsourced books and revising agent assignment processes to enhance quality and accountability.

Measuring Success: Our Progress by November 2008

By the end of October 2008, our transformation was showing results. Our liquidation ratio climbed to 24.88%, up from 23.99% in September, with 2,537 assets sold—a record level. Days REO dropped to 162, and days on market fell to 109, both better than the prior year’s figures. Our sales price to original anticipated sales price held steady at 91.91%, and net proceeds metrics improved, reflecting our focus on value recovery. These gains, while incremental, were significant in a market where many competitors were struggling to stay afloat.

Looking Ahead: Building for the Future

As we moved into late 2008, I remained focused on sustaining momentum. Our strategic objectives—hitting 3,000 monthly liquidations, reducing timelines, cutting costs by 15% from our 2008 baseline, and driving innovation—guided every decision. We continued to refine our processes, expand our regionalization efforts, and deepen our partnership with JPMorgan Chase. I believed that by staying agile, data-driven, and customer-focused, EMC’s REO division could not only survive the crisis but emerge as an undisputed leader in asset management.

This transformation wasn’t easy, and it required relentless effort from our entire team. But as I reflect on our journey, I’m proud of how we turned adversity into opportunity, leveraging the crisis to redefine what’s possible in REO management. Our work during this period laid the foundation for EMC’s future success, and I’m confident it positioned us to thrive in the years to come.

Now, I’ll share some personal anecdotes that highlight the challenges, triumphs, and human moments behind our REO division’s transformation. These stories, drawn from my perspective, offer a glimpse into the intensity of the time and the personal stakes involved.

The Late-Night Strategy Sessions

I’ll never forget the late nights in our Lewisville, TX, office, hunched over spreadsheets and market reports with David Little, our Executive Vice President, and a handful of key team members like Teresa Nixon and Dena Grimes. It was October 2008, and the news of Bear Stearns’ collapse and JPMorgan Chase’s takeover was still fresh. The pressure was immense—stakeholders demanded results, but the market was a mess, with property values dropping daily. One night, we stayed until 2 a.m. debating whether to push forward with our LenderMustSell.com pilot in California. I argued passionately for it, believing that mass marketing could cut through the noise and drive sales, even in a declining market. David, with his 25 years of experience, pushed back, worried about the upfront costs. But after crunching the numbers and seeing early web leads surge by 35%, we greenlit it. That decision became a cornerstone of our sales strategy, and I felt a surge of pride watching it pay off in the weeks that followed.

The Coffee-Fueled Field Visit

One crisp morning in late 2008, I flew out to Irvine, CA, to meet with Rod Telles and our West Coast team. I was exhausted—coffee had become my lifeline amid 12-hour workdays—but I knew I needed to see our operations firsthand. We visited a cluster of REO properties in a hard-hit neighborhood, where foreclosure signs dotted nearly every block. I walked through a vacant home with one of our property inspectors, Ryan Wiesemeyer, who’d just joined us. The place was a wreck—graffiti on the walls, broken windows—but Ryan’s enthusiasm for turning it around was infectious. He shared ideas for quick rehab strategies we could pilot in select MSAs, and I saw the potential to reduce loss severity. That day, over a rushed lunch of sandwiches, I scribbled notes on a napkin, sketching out how we could regionalize our approach to prioritize high-volume areas. It was a small moment, but it reminded me why I loved this work—the chance to solve real problems and make a difference, even in chaos.

The Team’s Resilience

There was a moment in November 2008, right after we rolled out new performance incentives for our asset managers, that tested our team’s spirit. We’d just learned that one of our top performers was leaving voluntarily, and morale dipped. I gathered our 87 employees in the Lewisville office for an impromptu meeting, sharing coffee and donuts I’d picked up on the way. I told them about my own doubts during the crisis—how I’d questioned whether we could hit our 3,000-sales-per-month goal or reduce timelines under 163 days REO. But I also shared my belief in their talent and our shared mission to lead the industry. I’ll never forget the applause that followed, or how Dena Grimes, newly promoted, stepped up with a plan to boost accountability through tighter agent assignments. That day, I saw our team’s resilience firsthand, and it fueled my determination to keep pushing forward.

The Personal Toll and Triumph

The crisis took a personal toll on me, too. I missed family dinners and my daughter’s birthday celebrations because I was buried in reports or on conference calls with Chase executives. One evening, after a particularly grueling day reviewing our October 2008 performance—2,440 assets sold, but still short of our stretched target—I stepped outside our office and called home. Hearing my daughter’s voice, excited about a school project, reminded me why I was doing this: to secure a future, not just for EMC, but for my family and others facing the same economic uncertainty. That call gave me the strength to return to my desk and finalize our strategy for regionalizing portfolios by geography and risk, a move that later slashed our costs and improved efficiencies.

The Quiet Victory

By December 2008, as we prepared to expand our national rehab program and adjust our outsource strategy, I had a quiet moment of victory. I was reviewing our latest liquidation numbers—up to 24.88% from the previous month—and realized we’d turned a corner. Sitting in my office, I looked at a photo on my desk of a Colorado hiking trip I’d taken before the crisis hit, a reminder of simpler times. I felt a deep sense of gratitude for our team’s hard work and for the innovative tools like LenderMustSell.com that were starting to show real results. It wasn’t a flashy milestone, but it was mine—a personal acknowledgment that we were not just surviving, but thriving, against all odds.

These anecdotes capture the highs and lows of leading EMC’s REO division through the financial crisis. They’re moments of grit, collaboration, and hope that shaped our strategy and reinforced my commitment to transforming our approach, no matter the challenges.

Leadership during crises, like the 2008 financial crisis we navigated, requires a blend of vision, adaptability, and resilience. Drawing from my experience managing the REO division during that tumultuous period, here’s an in-depth look at the principles and practices that defined effective leadership under pressure, tailored to the broader context of crisis management.

1. Vision and Strategic Clarity

In a crisis, leaders must provide a clear direction amidst chaos. When the housing market collapsed in 2008, I knew our traditional REO sales approach wouldn’t suffice. I set a bold vision to transform EMC into a portfolio manager and consumer service model, focusing on liquidating distressed assets while cross-selling JPMorgan Chase products. This vision wasn’t just aspirational—it was actionable, with specific targets like increasing liquidations to 3,000 assets per month and reducing REO timelines to under 163 days. I communicated this vision relentlessly to our 87-employee team, ensuring everyone understood their role in stabilizing losses and driving value recovery. A clear vision anchors a team, preventing panic and aligning efforts toward a common goal.

2. Data-Driven Decision Making

Crises are unpredictable, but data can provide stability. I relied heavily on analytics and market intelligence to guide our strategy. For instance, we tracked liquidation ratios, days REO, and sales price recoveries monthly, using October 2008’s 24.88% liquidation ratio and 162 days REO as benchmarks for improvement. When we piloted LenderMustSell.com and saw 35% of leads coming from web and email, I doubled down on digital marketing strategies. This data-driven approach allowed us to adjust our regionalization efforts, prioritize high-volume MSAs, and implement performance incentives, ensuring decisions were rooted in evidence rather than guesswork.

3. Adaptability and Innovation

The 2008 crisis demanded constant adaptation. Property values plummeted, foreclosure inventories swelled, and traditional methods failed. I embraced innovation, launching auction-style marketing, partnering with lender liquidation companies, and regionalizing our portfolio by geography and risk. When title issues and evictions slowed our timelines, we revised agent assignment processes, assigning listing agents immediately after boarding new REOs, and coordinated second BPOs to enhance valuation quality. These innovations, like our national rehab program piloted on outsourced books, weren’t perfect, but they kept us agile, allowing us to differentiate EMC from competitors and reduce costs by 15% from our 2008 baseline.

4. Empowering and Supporting Teams

A leader’s strength lies in their team’s resilience. I prioritized talent development, implementing training programs to equip our staff with crisis-specific skills and rolling out performance incentives to boost morale. When one of our top asset managers left voluntarily in late 2008, I held an impromptu meeting, sharing coffee and donuts with the team to rebuild confidence. I leaned on regional leaders like Teresa Nixon, Dena Grimes, and Rod Telles, empowering them to drive accountability and ownership in their areas. By fostering a culture of collaboration and recognition—such as promoting Dena to Assistant Manager for Alternative Disposition Services—we maintained momentum, even as the crisis tested our limits.

5. Stakeholder Communication and Trust

During a crisis, maintaining trust with stakeholders is critical. I worked closely with JPMorgan Chase executives, Bear Stearns remnants, and internal teams to align our REO strategy with broader corporate goals. Regular updates on our progress—such as reducing days on market to 109 by October 2008 or improving sales price recoveries to 91.91% of original anticipated values—built confidence. I also ensured transparency, sharing both successes (like record liquidations of 2,537 assets) and challenges (like declining property values hitting 49.72% of appraised values). This open communication fostered trust, ensuring stakeholders saw us as reliable partners in navigating the crisis.

6. Personal Resilience and Balance

Leading through a crisis takes a personal toll. I missed family moments—birthdays, dinners—because I was analyzing reports or strategizing late into the night. One evening, after a grueling day reviewing performance metrics, I stepped outside our Lewisville office, called home, and heard my daughter’s excitement about a school project. That brief connection reminded me why I was pushing so hard: to secure a future for my family and others. I leaned on coffee, long walks during field visits, and small rituals—like keeping a photo of a Colorado hiking trip on my desk—to maintain focus. Personal resilience isn’t just about endurance; it’s about finding purpose amidst exhaustion.

Broader Lessons from Crisis Leadership

Across industries, effective crisis leadership shares these traits. Historical examples, like CEOs navigating the 2008 recession or public health leaders during pandemics, show that success hinges on rapid decision-making, transparent communication, and team empowerment. However, leaders must also critically examine establishment narratives—such as over-reliance on traditional methods or optimistic forecasts that ignore market realities. During 2008, I questioned assumptions about REO sales, pushing for innovation over complacency, even when stakeholders resisted change.

Lessons from the 2008 Financial Crisis: Leading Loss Mitigation and REO Portfolios Today

As Matt Slonaker, I’d bring hard-earned lessons to running a loss mitigation and REO portfolio at a large bank or mortgage servicer today. The challenges of distressed assets, plummeting property values, and stakeholder pressure remain relevant, but the technological landscape has evolved dramatically since 2008. Here’s how I’d approach leadership today, drawing on those lessons and leveraging modern AI and tech tools I didn’t have back then.

Key Lessons from 2008 Applied Today

1. Vision and Strategic Agility: A Data-Driven, Customer-Centric Approach

Back in 2008, I transformed EMC’s REO division into a portfolio manager and consumer service model, targeting 3,000 monthly liquidations and reducing REO timelines to under 163 days. Today, I’d maintain that focus on agility but enhance it with a sharper, data-driven vision. I’d prioritize aligning loss mitigation and REO strategies with broader bank goals—like cross-selling financial products or retaining customers—while anticipating market shifts, such as rising interest rates or regional housing downturns.

Use Case for AI/Tech: I’d deploy AI-powered predictive analytics to forecast market trends and property value declines in real time. For example, an AI model could analyze macroeconomic data, local housing inventories, and borrower credit profiles to predict which loans are likely to default, allowing us to proactively offer loss mitigation options like loan modifications or short sales. Tools like Zillow’s Zestimate or Redfin’s data APIs, combined with machine learning, could provide granular insights into REO property valuations across MSAs, enabling faster, more accurate pricing decisions than our manual BPOs in 2008.

2. Timeline Management: Streamlining Operations with Automation

One of our biggest challenges in 2008 was reducing REO timelines—162 days on average by October 2008, with evictions and title issues causing delays. Today, I’d double down on process efficiency, targeting timelines under 120 days through automation and real-time tracking.

Use Case for AI/Tech: I’d implement robotic process automation (RPA) to handle repetitive tasks like agent assignments, BPO coordination, and eviction scheduling. An AI chatbot integrated with our CRM could manage initial customer interactions for loss mitigation, guiding borrowers through options like forbearance or deed-in-lieu programs 24/7. Blockchain technology could streamline title transfers and resolve issues faster, reducing delays we faced in 2008. Real-time dashboards powered by AI could monitor key metrics—liquidations, days REO, sales price recoveries—alerting me to bottlenecks instantly, unlike the weekly reports we relied on back then.

3. Cost Reduction and Value Recovery: Leveraging Tech for Precision

In 2008, we aimed to cut costs by 15% and enhance value recoveries to over 68% of pre-foreclosure BPO values. Today, I’d use advanced tech to achieve these goals more precisely, especially in a market with fluctuating property values.

Use Case for AI/Tech: AI-driven property valuation tools, like those from CoreLogic or Black Knight, could analyze historical sales data, neighborhood trends, and satellite imagery to set optimal listing prices for REO assets, reducing loss severity (e.g., our 49.72% sales price to appraised value in October 2008). I’d also use AI to identify rehab opportunities, analyzing images and structural data to recommend cost-effective repairs, boosting sales prices in select MSAs. Drones and IoT sensors could monitor property conditions in real time, minimizing preservation costs we managed manually with inspectors back then.

4. Talent Development and Innovation: Upskilling for a Tech-Driven Era

We invested in training our 87 employees in 2008, but today’s workforce needs digital fluency. I’d ensure our team is skilled in AI tools, data analysis, and customer engagement platforms to stay competitive.

Use Case for AI/Tech: I’d use AI-powered learning management systems (LMS) to deliver personalized training on loss mitigation strategies, REO sales techniques, and tech tools. Virtual reality (VR) simulations could train staff on property inspections or customer negotiations, replicating real-world scenarios we handled in person in 2008. AI chatbots could handle routine inquiries, freeing staff to focus on strategic tasks, unlike the manual customer service we provided back then.

5. Stakeholder Communication: Real-Time Transparency

In 2008, I maintained trust with JPMorgan Chase and internal teams through regular updates on metrics like our 24.88% liquidation ratio. Today, I’d use tech to provide real-time transparency and foster collaboration.

Use Case for AI/Tech: I’d deploy a cloud-based dashboard, powered by AI analytics, to share live performance data with stakeholders—liquidations, cost savings, value recoveries—accessible via mobile devices. Natural language processing (NLP) tools could generate automated reports, summarizing trends and risks in plain language, reducing the manual effort I spent compiling updates. This would build trust faster than our monthly meetings in 2008, especially in a crisis.

Specific Strategies for Today’s Market

- Proactive Loss Mitigation: I’d use AI to identify at-risk borrowers early, offering tailored solutions like payment deferrals or loan restructures. For example, an AI model could analyze payment histories, employment data, and local economic indicators to flag potential defaults, then recommend mitigation options via a mobile app, unlike our reactive approach in 2008.

- Dynamic REO Pricing: With AI and big data, I’d dynamically price REO assets based on real-time market conditions, bidding wars, and buyer demographics, avoiding the static BPOs we relied on. This could increase sales prices to over 92% of anticipated values, surpassing our 91.91% in October 2008.

- Regional Optimization: I’d regionalize portfolios using geospatial AI, segmenting by zip codes and risk levels to prioritize high-volume areas, reducing costs and improving efficiencies beyond our 2008 efforts. Drones could survey properties in rural or hard-to-reach areas, cutting inspection times and costs.

- Customer-Centric Cross-Selling: I’d use AI recommendation engines to cross-sell bank products (e.g., mortgages, insurance) to REO buyers, leveraging CRM data to personalize offers, a step beyond our 2008 cross-selling initiatives with Chase.

Challenges and Considerations

While these tools are powerful, I’d critically examine their limitations. AI models can perpetuate biases if trained on flawed data, so I’d ensure diverse datasets and human oversight. Privacy concerns, like GDPR or CCPA compliance, would require careful data handling, unlike the less regulated environment of 2008. Finally, I’d balance tech adoption with human judgment, avoiding over-reliance on automation, as I learned the value of personal relationships and team morale during the crisis.

interested to learn and explore more around this key topic, then let’s meet!

Regards,

Matt

NICE TO MEET YOU

I'm Matt Slonaker

As the Founder of M. Allen, I empower B2B companies to achieve breakthrough sales in half the time. Leveraging strategic insights, proven methodologies, and a robust network, I have produced or overseen $200 million in new revenue opportunities for stakeholders.

With experience as a revenue, financial services C-suite executive leader, and a U.S. Navy combat veteran, I bring resilience and strategic insight to every project. My results-driven approach ensures that your goals are met and exceeded.